How to Avoid Miscalculating the First-Year Applicable Fraction

By Mahoney

In the first year of a tax credit project, the applicable fraction is calculated differently than subsequent years. Calculating the applicable fraction for first-year low-income housing tax credits isn’t quite as easy as taking the months a building is in service divided by 12 months.

The IRS Explanation

Described in IRC §42(f)(2)(A), the special rule for the first year of the tax credit period is calculated by using the sum of the applicable fractions for each month (determined at the last day of each full month) of the taxable year the building was placed in service as the numerator, and the denominator is 12, for the total number of months in the year. The result of this will be an “averaged” applicable fraction that accounts for the period that the units were not yet placed in service or available for occupancy. See the example below for how to calculate the applicable fraction for each month of the year the building was in service.

An Illustrated Explanation

To provide a more descriptive example of how to calculate the first-year applicable fraction, consider the following scenario:

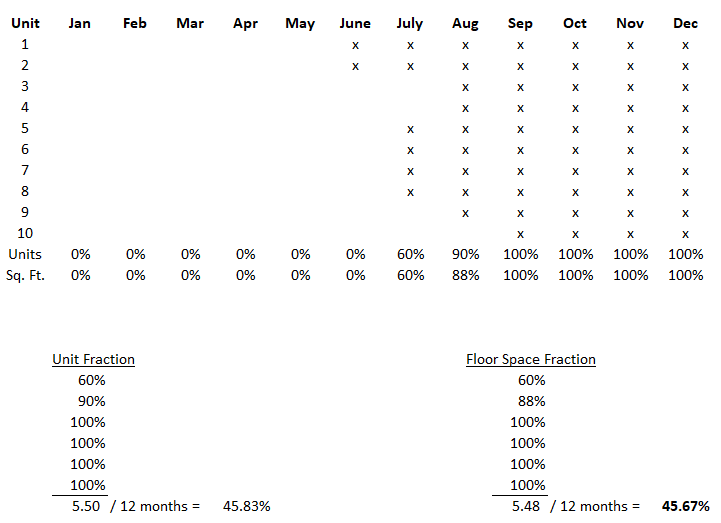

A newly constructed IRC §42 building containing 10 low-income units is occupied by qualified tenants and placed in service June 25, 2020. This makes the year 2020 the first year of the credit period. Units 1-5 are 1,000 square feet and units 6-10 are 1,500 square feet, with a building total of 12,500 square feet. The chart below illustrates when units were placed in service and the appropriate credit applicable:

Even though there were two tenants occupying units in June, the applicable fraction for that month is zero. The building must be placed in service for the entire month to get credits. July is the first full month placed in service with qualified tenants occupying units, so it is the first month that will have an applicable fraction greater than zero.

The applicable fraction for this building’s first-year credits is the smaller of the unit fraction or the floor space fraction. In this scenario, the applicable fraction will be 45.67%, or the floor space fraction.

Common Computation Mistakes to Avoid

- When computing the first-year applicable fraction, remember it is not just based on the month the building was placed in service. If the building was placed in service in July, the applicable fraction is not six months ÷ 12 months. You must compute the unit fraction and the floor space fraction for each month to determine the weighted average.

- Be certain to compute both the unit fraction and the floor space fraction. Both fractions must be calculated to determine the lesser fraction and ensure the correct applicable fraction is being used.

- Don’t be tempted to include a partial month of occupancy in the applicable fraction calculation. To include a unit in the applicable fraction, it must be placed in service for the entire month and occupied at least one day of that month.

As we have demonstrated above, the calculating of the first-year applicable fraction for a low-income housing tax credit can be open to miscalculation. For this reason, it may be valuable to consult with qualified accounting experts experienced in these matters for support and consultation.

For additional considerations, please reach out to Megan Brownell, Associate, or contact our Real Estate Solutions Team at Mahoney to be of help to you in any way.