For many not-for-profits, 2020 was the year of revenue recognition implementation. One of the most prevalent challenges I noticed for many not-for-profits was remembering revenue recognition consisted of implementing two accounting standards, not one. So, the first step for implementation was determining which standard their revenue should be recognized under.

While there are potentially more standards for revenue at not-for-profits to be recognized under, the two new standards in 2020 were 2014-09 Revenue from Contracts with Customers (Topic 606) and 2018-08 Clarifying Accounting Guidance from Contributions and Grants.

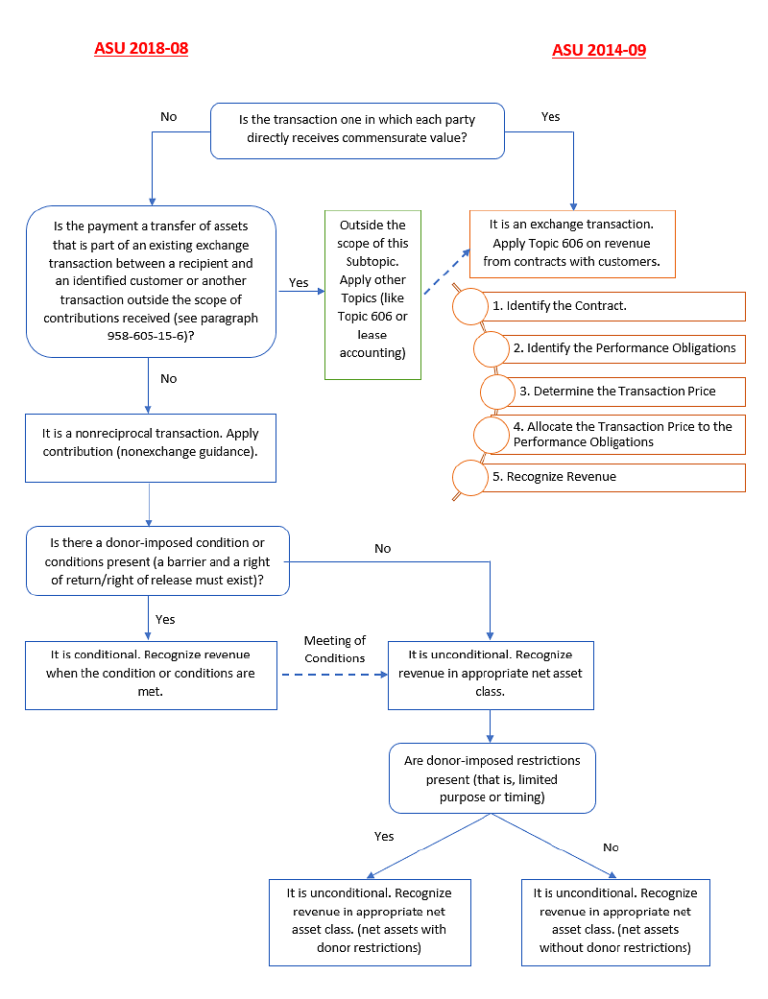

The flowchart listed below helps not-for-profits identify how to report revenue depending on the type of revenue received.

The Most Important Step is the First One

Management at many of the not-for-profits I worked with made a concerted effort to prepare for these new standards and understood the steps to determine how to recognize revenue under each standard. The problem came when they tried to apply the steps from ASU 2014-09 to a government grant which was actually a contribution or tried to apply ASU 2018-08 to a program service fees. Management would get into a groove performing the steps from ASU 2018-08 on all their government grants, asking “Are there conditions?”, “Are there restrictions?”, etc., and apply these to all of their agreements with government agencies, even though one was a reciprocal agreement that actually fell under ASU 2014-09 or vice versa.

In many situations these two methods came to the same result regarding when to record revenue, but that was not always the case. Since the supporting determination process and documentation was not correct; we did not know for certain that the revenue recognized was the same until the correct determination process was performed. Even if the amount of revenue recognized was correct, the disclosures were all wrong.

Revenue Recognition Example

Let’s say a client had a government contract to provide training to the State’s employees. The state would reimburse them for the time and costs to prepare the material and provide the classes. This is a reciprocal agreement and should be recorded under ASU 2014-09. However, all the Organization’s other government grants are conditional contributions so when they looked at this government contract, they kept using the same process they had been using under ASU 2018-08. They determined that under ASU 2018-08, the Organization had to provide XX number of classes by December 31 to meet the conditions and therefore should not record any revenue until the last class was provided.

Under ASU 2014-09, which would be the correct accounting standard to be used in this situation, they earned the revenue prorated over the term of the agreement; during planning, designing and then providing the classes. Since the client operated on a June 30, 2020 year end, the revenue recognition was materially different as all receipts to date under the ASU 2018-08 determination were recorded as refundable advances. Under ASU 2014-09 it was all revenue.

While a single miscoded agreement may not be material to the financial statements, multiple errors can add up to be a problem. You will not know until you make the proper determination.

These Standards Are Here to Stay

You may think now that implementation has happened this will not be an issue any more, but these standards are here to stay. Every time a not-for-profit gets a new grant or signs a new contract, they will need to perform these determinations. It is important to remember there are two standards (or more) for not-for-profits to be recording revenue under, and the first step is to figure out which standard the revenue is under before going any further.